Sam Makad

Sam Makad is a business consultant. He helps small & medium enterprises to grow their businesses and overall ROI. You can follow Sam on Twitter, Facebook, and Linkedin.

AI is emerging as a powerful ally in the fight against fraud. Financial services leverage the power of AI to keep customer money and data safe - find out how

From insurance to banking, the finance industry relies on trust. Customers need to know that their money and their data are in safe hands and will not be leaked to cyber criminals. Fraud prevention and mitigation are, therefore, top priorities. But as cybercrime continually evolves, traditional fraud detection methods struggle to keep up.

In the fight against financial fraud, a powerful player has emerged in recent years: AI. Artificial intelligence is revolutionizing the entire landscape of fraud prevention.

In this article, we explore the various ways financial services are leveraging AI to combat fraudulent activity.

Artificial intelligence (AI) means a machine’s ability to perform functions that we usually associate with human minds and cognition, such as perception, processing and generating language, and interpreting data.

You’ll likely already be familiar with AI in some form or other – especially as ChatGPT becomes more widely used in tech and other industries. But what do we mean when we talk about AI in the context of fraud detection?

AI fraud detection means using computer algorithms and AI models to learn from historical data and detect new patterns and anomalies that could be indicative of fraudulent activity. AI-based systems are called upon to detect fraud across multiple industries, from retail to healthcare, but it is possibly making the biggest waves in the world of financial services.

Artificial intelligence has many uses – and is not without controversy – is it ethical, for example, to use AI tools for copywriting?

In finance, its uses range from the protection of assets to customer care. In fact, organizations are increasingly exploring innovative solutions, like creating a bot with GenAI to enhance customer interactions and bolster fraud prevention efforts.

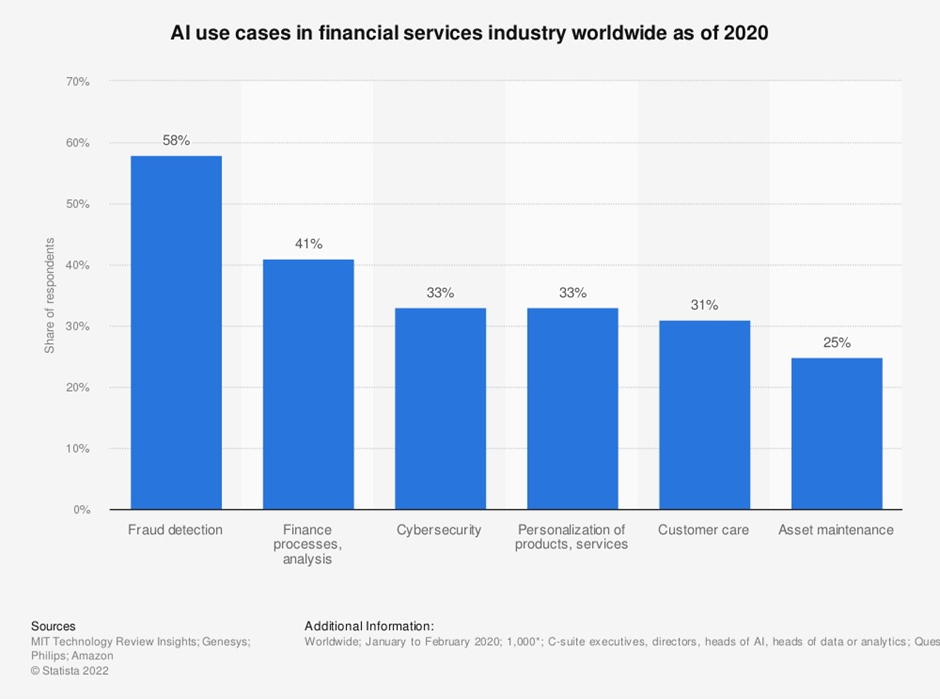

Its most important job, though, is protecting against fraud. As of 2020, 58% of the financial industry relied on AI for fraud detection.

Image sourced from statista.com

Why is this?

Since banking firms, insurance companies, and related organizations are dealing with huge amounts of data, it makes sense to leverage the processing power of computer algorithms. AI-based fraud detection systems are renowned for fast detection and increased accuracy – both of which are essential in the finance industry, where stakes are high.

Imagine you’re reviewing a loan application. All the documents seem to be in order, and there’s nothing to suggest that the candidate is unsuitable. To the naked human eye, nothing is wrong.

Except, the application has been doctored. This is a fraudster who will take your funds and never be seen again. Loan fraud can sink your business if you don’t protect yourself.

This is why so many banks are adopting AI to detect suspicious activity. Of these banks, 60% say that AI is their most important tool in fighting fraud.

So, how exactly is AI helping to fight against fraud? What is it about artificial intelligence which is beneficial in the finance industry? Let’s look at the qualities of artificial intelligence that make it suited to the task.

Humans aren’t typically wired to make sense of huge quantities of data without tools to help with the job. If you’ve ever used a data engineering platform, you’ll be familiar with machine learning being used to analyze raw data and generate actionable insights.

This is essentially the idea behind using AI to fight fraud. AI can be used for automated anomaly detection. As machine learning systems can sift through vast datasets in record time, they can quickly and efficiently spot irregularities that human analysts would likely overlook.

Pattern recognition skills are hugely beneficial in financial services. Think unusual transaction amounts, multiple transactions from the same device, or multiple purchases made from separate locations back to back. AI-powered systems can spot when a transaction does not fit the pattern and raise red flags for further investigation.

AI's potential for pattern recognition goes beyond simply crunching numbers in datasets. Over time, artificial intelligence can also analyze customer behavior.

By establishing a baseline of normal behavior for a user, AI technology can spot if a customer suddenly starts acting erratically, making uncharacteristic purchases that do not tally with their usual spending habits.

Based on its knowledge of user behavior, AI can flag transactions as suspicious and even block further actions until the user’s identity has been verified. This is great news when it comes to stolen credit cards, as even if the thief tries to mimic the original owner’s spending, AI will detect a change in the complex pattern which is human behavior.

Free for use image sourced from Pixabay

Natural language processing (NLP) is the branch of computer science concerned with giving AI the ability to understand text and spoken word. This is the technology behind chatbots and similar innovations currently taking the internet by storm.

AI algorithms can use NLP to analyze text-based customer communications, such as emails or chat transcripts. AI-based chatbots can identify suspicious requests, phishing attempts, and other potential scams.

As AI continues to develop, we may see NLP being put to use in monitoring logs and phone data – further protecting customer data from human interference and fraud.

Additionally, machine learning technology means that AI is often able to identify new fraud patterns by learning from emerging data. This adaptability is important because it means that AI can keep up with fraudsters’ evolving tactics. In the long run, this means that AI-based fraud detection systems are most likely here to stay, as they won’t become outdated in the near future.

Traditional methods of fraud detection rely on manual processes, which can, of course, be time-consuming. AI is at a significant advantage because of its ability to operate in real-time. AI algorithms can assess transactions instantly to identify potential fraud.

This is key as it’s imperative financial organizations can move fast – faster than a criminal can destroy your funds. If a financial institution can detect fraud in real-time, they can mitigate damage – thereby fostering trust in their customers and keeping their reputation as a trustworthy institute spotless.

In addition to leveraging AI's real-time detection alongside comprehensive log monitoring is key to swiftly identifying fraudulent activities. Log monitoring systems play a critical role in collecting, analyzing, and interpreting system logs to detect unusual patterns and potential threats.

They complement AI-driven fraud detection efforts by providing additional insights into system performance and user activities. Institutions can gain a more holistic view of their security landscape by understanding the importance of log monitoring and its role in strengthening financial security. This combination of AI and efficient log monitoring ensures better detection and prevention of fraud, thereby enhancing overall security measures.

Many AI-powered solutions work in tandem with machine learning (ML).

Machine learning is a subfield of artificial intelligence focused on developing algorithms and models that enable computers to learn from data. This means that they can make predictions and decisions without being specifically programmed.

Free for use image sourced from Unsplash

Now you know the features of Artificial Intelligence that make it such a powerful tool in fighting fraud: its abilities, such as pattern recognition, behavior analysis, NLP, and continuous learning, make it a huge asset to financial firms.

Now, how do AI-powered fraud detection systems work? The answer is that they run on algorithms.

In rule-based fraud detection (more on this to come), humans program the system with the appropriate rules, and AI sorts through the data according to these rules.

In more advanced systems, AI is used in combination with machine learning algorithms, which we have just discussed. The two work in tandem to reduce fraud risk, as not only can they identify existing trends in the data: but they can also ‘learn’ new patterns.

First, use an ETL data pipeline to move data from multiple sources into a secure data lake. It all starts with the machine learning algorithms analyzing and segmenting this data to extract required features. The more data they can learn from, the better.

Then, feature extraction is used to determine legitimate customer behavior patterns vs. fraudulent ones. A training algorithm launches and sets rules for identifying between the two. After the training is over, it generates an improved machine-learning algorithm that can better detect fraud.

Here are some examples of the types of algorithms used for AI fraud detection:

These look for specific characteristics of known fraud based on human input. They can only detect types of suspicious activity that they have been programmed to recognize – they cannot learn as they go. As a result, they require constant updating and manual intervention to correct errors.

As mentioned above, ML algorithms are more advanced. As well as learning from past experiences, they also continue adapting to the data and can make predictions about future outcomes.

Supervised learning models require training using tagged (labeled) data, which is fed into the model to create a prediction. Accuracy varies – it depends on how well-organized your data is. Data-driven organizations will have a much easier job of managing data.

Instead of relying on tagged data, unsupervised learning models identify clusters of similar items by analyzing unlabeled data. Supervised and unsupervised learning can both be used independently or together to pick complicated patterns and detect fraud.

Onto the most complicated: deep learning algorithms. With many layers and nodes, deep learning algorithms are like neural networks working at multiple levels to handle huge amounts of data and perform real-time analysis.

This is achieved by looking at the content of the transaction in detail, analyzing the amount, type, and source of payment - as well as timestamps and other factors. This is used to determine whether someone is trying to make unauthorized purchases, steal card information, or commit identity theft.

Let’s look at a practical example: how is AI helping to fight fraud in the banking industry, specifically?

Free for use image sourced from Pixabay

We’ve mentioned that artificial intelligence is useful for reducing human error and catching flaws at scale. For this reason, more and more banks are adopting AI and machine learning to help them identify suspicious transactions in real-time.

AI fraud detection is also useful when it comes to loan applications from bad actors. By scanning documents to analyze metadata and pixel-level information, AI can ensure the integrity of a document. Whether it’s a fake bank statement, stolen personal identification details, or an otherwise manipulated financial document, AI-software can find subtle variations in font and layout that indicate fraud.

This level of scrutiny is particularly important in a world where tax regulations are becoming increasingly complex, and financial institutions must not only protect against traditional fraud but also navigate the intricacies of tax compliance across different states. For example, economic nexus rules state that if a business sells a certain amount of products or services in a particular state, they have to collect and pay taxes in that state, even if they don't have a physical store or office there.

Fraud prevention is a company-wide effort. Bank applications should pass many stages of processing before approval. Artificial intelligence is great for catching any signs of fraud that are invisible to the naked eye.

AI also plays a key role in fraud detection within the insurance industry.

Without AI, insurance companies spend days or even weeks assessing every single claim - whether it's a property damage case, car accident, or unemployment claim - looking for potential insurance fraud.

AI comes in to reduce time or human error. However, human-knowledge-based AI is not enough. Insurance firms tend to use more advanced machine learning models with the capacity for semantic analysis to detect false claims.

Free to use image sourced from Pixabay

Fighting fraud in financial services is an ongoing challenge. However, AI is driving a revolution in the way financial institutions detect and combat fraudulent activity with speed and accuracy previously unheard of.

AI is perfect for helping to fight fraud because it excels in pattern recognition, including behavioral analysis and complex formations that humans may miss. It works in real-time, using natural language processing skills and machine learning abilities.

Leveraging the power of machine learning models in conjunction with artificial intelligence, institutions can improve online security, protecting their customer’s money and data while maintaining their own reputation and integrity.

To conclude: fraud continues to evolve, but so does AI. Its role in fraud prevention, especially in the finance industry, will undoubtedly continue to grow in the future.

You’ll also receive some of our best posts today

Sam Makad is a business consultant. He helps small & medium enterprises to grow their businesses and overall ROI. You can follow Sam on Twitter, Facebook, and Linkedin.

The whole world has gone online, and so did...

College years are a fascinating time for the majority...

User reviews are a game-changer for e-commerce. Consumers rely heavily o...

Don’t miss the new articles!